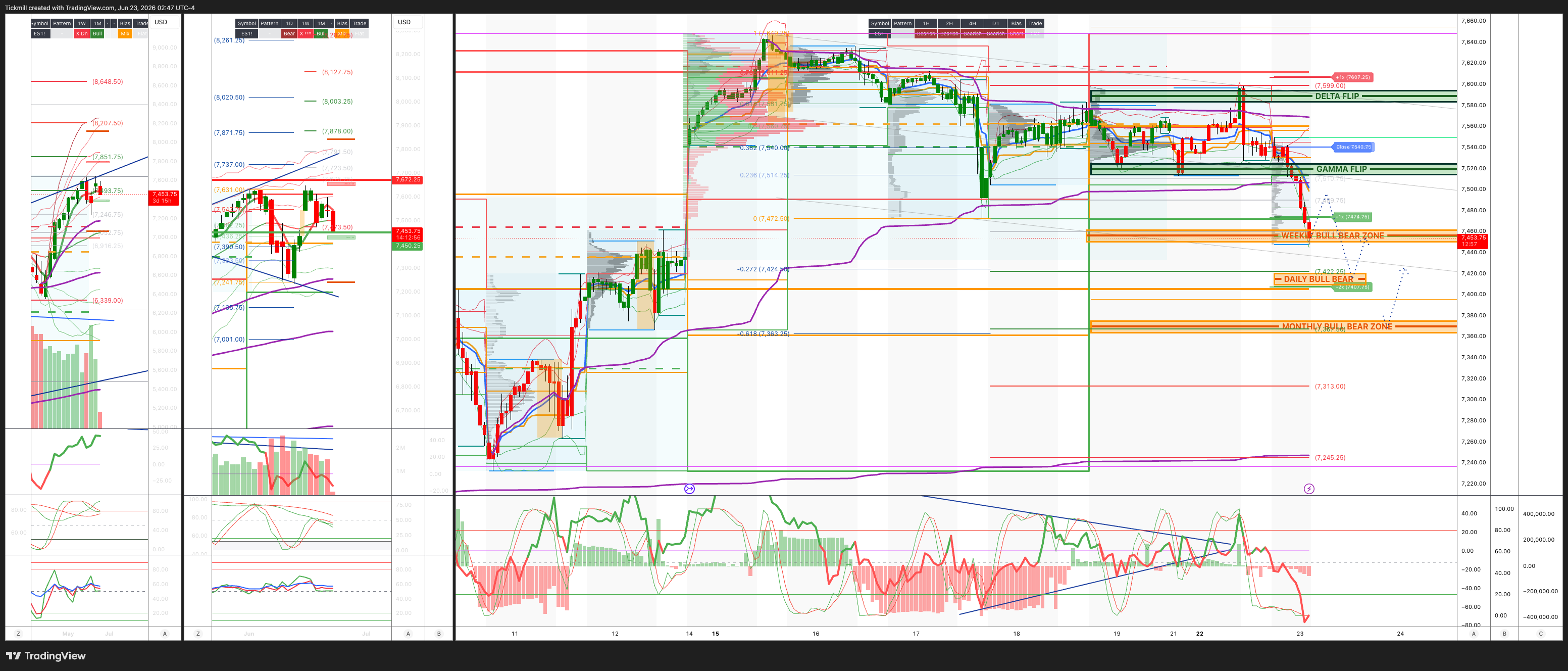

S&P500 Daily Action Areas & Price Targets 23/6/26

S&P500 Daily Action Areas & Price Targets 23/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7560/50

WEEKLY RANGE RES 7692 SUP 7448

MONTHLY RANGE RES 7932 SUP 7384

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.22 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BEARISH 7573

WEEKLY VWAP BULLISH 7494

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - BALANCE 7599/7527

WEEKLY STRUCTURE - BALANCE 7648/7247

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 77410/20

GAMMA FLIP 7522

DELTA FLIP 7588

DAILY RANGE RES 7608 SUP 7472

2 SIGMA RES 7676 SUP 7404

VIX BULL BEAR ZONE 17.4

TRADES & TARGETS

LONG ON REJECT/RECLAIM WEEKLY BULL BEAR ZONE TARGET 7500>CLOSE

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET WEEKLY BULL BEAR ZONE

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Slow Start’

Yesterday was a slower post-holiday session, but the under-the-hood message was more interesting than the index move. The S&P slipped 37bps to 7,473, NDX fell 19bps to 30,347, while the Russell gained 86bps to 3,005 and the Dow rose 29bps to 51,713. Volumes were still elevated at 22.94bn shares versus a YTD daily average of 19.5bn, though floor activity was quiet at 3 out of 10. The MOC was $1.6bn to buy, which helped stabilize the close, but the desk finished meaningfully better for sale versus the 30-day average. So the headline tape was soft, but not disorderly.

The key theme remains rotation rather than broad de-risking. Momentum broke out to new all-time highs, Semis were broadly strong, Russell and equal-weight proxies outperformed, while weakness in several megacaps acted as a source of funds. This fits the recent Prime Brokerage data showing Mag 7 gross and net exposure down to one-year lows, even as broader US Tech exposure has moved toward five-year highs. Investors are not abandoning AI; they are moving deeper into the AI ecosystem, especially Semis, Semi Equipment, memory, and Asian chipmakers, instead of simply adding more Mega-Cap exposure.

GOOG/GOOGL was the standout weak point, down about 6%. The cited catalyst was the departure of a lead DeepMind scientist to Anthropic, following last week’s disclosure that Noam Shazeer, co-lead of Gemini, would leave for OpenAI. The move magnitude does look extreme relative to the headline, but it highlights the market’s sensitivity to AI talent mobility and perceived platform risk. In the current environment, investors are increasingly willing to penalize hyperscalers or platform companies if they see evidence that AI leadership is less durable, talent retention is weakening, or capex intensity is rising without clear monetization.

That said, the GOOG selloff also looks like a useful example of rotational source-of-funds pressure. In a market where investors want more Semis and more direct AI infrastructure exposure, large-cap platform names can become funding sources, especially if there is any company-specific negative headline. This does not mean the Mega-Cap AI story is broken, but it does suggest that the market is becoming more discriminating inside Tech. “AI exposure” is no longer enough; investors are differentiating between capex beneficiaries and capex funders.

The strength in Semis was more important than the weakness in GOOG. Tech flows again skewed better to buy in Semis, most notably in Semi Equipment. That reinforces the idea that investors continue to prefer the physical infrastructure layer of AI: chips, memory, tools, equipment, networking, and supply-chain beneficiaries. MU earnings Wednesday after the close are therefore a key catalyst. Given the recent strength in memory and AI hardware, the bar is likely high, but if MU confirms demand strength, pricing, HBM momentum, and capex discipline, it can support the broader AI infrastructure complex.

Biotech was another notable green shoot, up about 4% after the APGE-ABBV deal and other clinical updates. This matters for the broadening narrative. Healthcare had recently screened as underweight in positioning data, and Biotech has been a laggard for a long time. Any pickup in M&A or credible clinical catalysts can attract capital because the sector is under-owned and less tied to the crowded AI trade. Biotech strength alongside Russell outperformance suggests some appetite for idiosyncratic risk is returning.

Small caps also had a better day, with R2K up 86bps. The Russell rebalancing effective Friday close may be contributing to activity, but the broader point is that non-Mega-Cap parts of the market are showing relative resilience. This is consistent with the recent data showing systematic positioning not stretched, discretionary sentiment still cautious, and many cyclicals under-owned. The challenge for small caps remains the macro backdrop: the 10-year rose 5bps to 4.51%, and Warsh’s Fed has made front-end policy uncertainty more important again. Small caps can participate in broadening, but they need rates volatility to stay contained.

The macro backdrop was mixed. WTI fell another 214bps to $74.23, extending the oil disinflation tailwind. That remains the key offset to the hawkish Fed impulse. Lower crude helps reduce headline inflation risk, supports consumers, and gives equities some cushion against higher yields. But the 10-year backing up to 4.51% and DXY firming to 101.02 show that the market has not fully dismissed Warsh’s hawkish debut. Gold rising 85bps to 4,192 alongside higher yields and a stronger dollar also suggests some residual demand for hedges or geopolitical/policy uncertainty protection.

VIX rose 310bps to 17.31, which is still not elevated in absolute terms but is notable given the relatively small SPX decline. This fits the broader theme of rising volatility beneath the surface. The market is not cracking, but large-cap Tech dispersion, NDX/SPX vol spread widening, RUT vol demand, and event-risk repricing are all signs that investors are paying more attention to convexity. The implied move through the end of the week is 1.3%, which feels reasonable given MU earnings, Russell rebalancing, post-FOMC rate sensitivity, and ongoing Tech rotation. So the implied range is approximately: SPX 7,376 – 7,570

Derivatives confirmed the broadening theme. NDX finished red, RUT finished green, and RSP reflected broader participation. SPX fixed-strike vols were little changed, while both RUT and NDX vols were bid. RUT spot and vol outperformance, especially in the front and belly of the curve, suggests investors are either chasing small-cap upside with optionality or hedging into event/rebalance risk. NDX skew notably outperformed SPX as the implied vol spread continues to blow out, consistent with the market assigning more downside/dispersion risk to Tech than to the broader index.

The desk’s interest in convex NFLX one-month and three-month call spreads makes sense tactically. NFLX was dragged down by Google/A24 investment headlines, and if that pressure is more narrative-driven than fundamental, call spreads offer a defined-risk way to play recovery without overpaying for outright upside. Similarly, buyers of Google upside structures on spot weakness suggest some investors view the 6% drawdown as overdone and are willing to fade the talent-departure panic using options rather than outright stock.

The corporate blackout period is now a real market-structure headwind. With an estimated 65% of issuers already in blackout windows ahead of Q2 earnings, buyback support is fading and will remain reduced through late July. This matters because buybacks have been an important stabilizer in a market with thin liquidity and elevated leverage. With corporate demand less present, flows from ETFs, systematic strategies, options hedging, and retail become more important in driving short-term price action.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!