Institutional Insights: Deutsche Bank - Investor Flows & Positioning 27/4/26

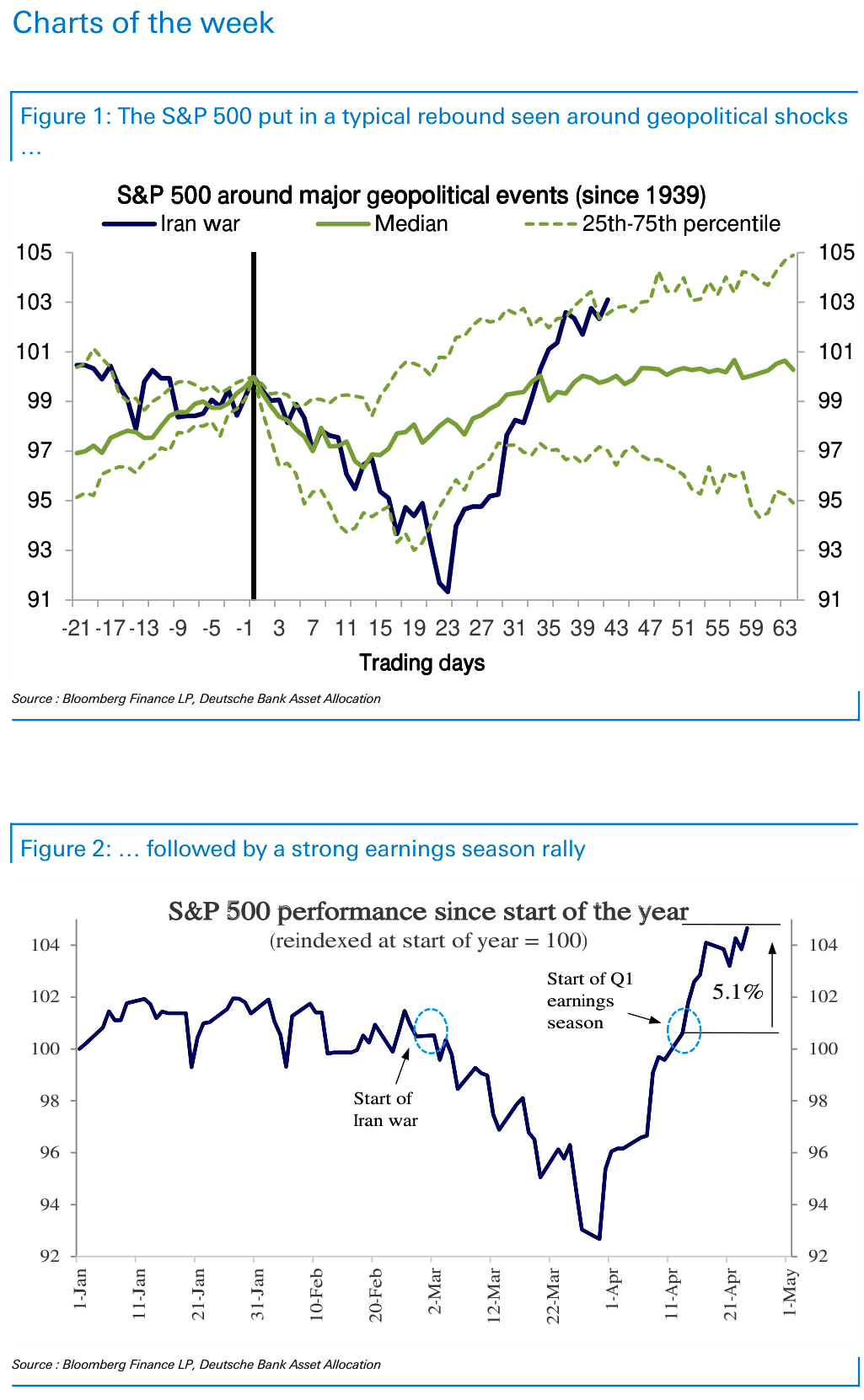

The April equity rally has transitioned cleanly from a geopolitical-shock recovery into an earnings-led advance. The first phase followed the classic post-shock template—a full V-shaped recovery within roughly six weeks after the Iran-War selloff—while the second phase has been supported by Q1 results, with the S&P 500 gaining another 5% over the past two weeks versus the roughly 1% typically seen at this stage of the earnings season. Despite the speed of the move, the rally does not yet look overextended. It appears more like a positioning catch-up after exposure had become sharply disconnected from earnings growth, which is now tracking near 21% year-on-year and above already-strong expectations.

Positioning remains supportive rather than euphoric. Aggregate equity positioning has moved from underweight to modestly overweight, but at only 0.29 standard deviations, or the 59th percentile, it still leaves room for further upside. Systematic investors have continued to rebuild exposure, but the process should remain gradual as recent volatility rolls out of lookback windows. Discretionary investors are also attempting to break above the cautious range that has capped exposure for more than a year, though positioning remains low relative to earnings growth—even when excluding megacap growth and technology. This suggests the rally can continue to grind higher if earnings revisions hold and macro shocks remain contained.

Demand-supply dynamics also remain constructive. Equity fund inflows continue to defy the usual seasonal slowdown, with $26bn of inflows this week led by $18bn into U.S. equities, alongside strong broad-global and EM demand. Regional flows are more mixed, with outflows from China, Korea, Europe and Japan, but the broader equity allocation impulse remains positive. Corporate demand is another key support: S&P 500 companies have announced $84bn of buybacks so far in April and more than $400bn over the past three months, with actual repurchases likely to follow. Technically, the S&P 500 remains below its strong 3.5-year trend channel and only mid-range in its post-GFC channel, while mega-cap growth and tech have only recovered from the bottom to the middle of their long-run relative trend.

Trading takeaways: stay tactically constructive on U.S. equities, with a preference for upside expressions that benefit from continued positioning catch-up rather than chasing outright beta indiscriminately. Mega-cap growth and technology can still lead if earnings momentum persists, but the better risk-reward may be in call structures, quality growth, and beneficiaries of ongoing buyback demand. Systematic re-risking and discretionary under-positioning argue against fading the rally too early, though month-end rebalancing, central-bank meetings and earnings concentration create near-term volatility risk. Regionally, favor U.S. and broad EM exposure over Europe and Japan, while using pullbacks around macro events to add rather than reduce equity risk unless earnings breadth or forward guidance deteriorates materially.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!