Institutional Insights: UBS 'SPX Short Gamma Into Month End'

Short Gamma Into Month-End

The market is entering month-end in a short-gamma regime, meaning dealers and other market participants are forced to sell into weakness and buy into strength, amplifying directional moves. At present, the setup appears short gamma on the upside, which creates the potential for an outsized rally early this week if any risk-on catalyst emerges.

The positioning stems from two sources: dealer options exposure and extreme short delta-one overlays in futures and ETFs.

In options, there is approximately $25bn notional of open interest in SPX March 31 6475 puts that dealers are short. At a current delta of roughly 75%, that translates into around $19bn of short SPX futures held as hedge. If SPX rallies back above 6475 into month-end, dealers may need to buy back those futures quickly, which could add significant fuel to any upside move—especially in a low-volume tape where even modest flows are moving the index disproportionately.

In delta-one, investors have reduced net exposure through futures and ETFs as elevated implied volatility has made options hedging more expensive. Because gross exposure remains high, many have chosen to protect P&L by adding shorts rather than cutting overall risk. That has left positioning notably short, particularly in RTY futures, and has also pushed crowded short expressions lower, increasing squeeze risk if sentiment improves.

Still, short gamma alone is not enough. The market needs a catalyst. That could come from a headline, month-end buying, lower oil, or simply a pause in selling. If such a spark appears, the current positioning could materially accelerate the upside move.

At the same time, risk parity remains the more important systematic downside risk. Rising bond/equity correlation has already triggered de-risking through much of March. CTA selling looks less pressing for now, as positioning is already short and sell triggers are still distant. Risk parity, by contrast, still has room to unwind further: with leverage around 71%, a roughly 3% decline in SPX could trigger about $100bn of additional selling.

For those looking to hedge a de-escalation right tail, Aaron Nordvik prefers the UBXXCUT Rate Cut Winner Basket, as well as upside optionality in XHB, ITB, and KRE, all of which remain levered to front-end rate repricing.

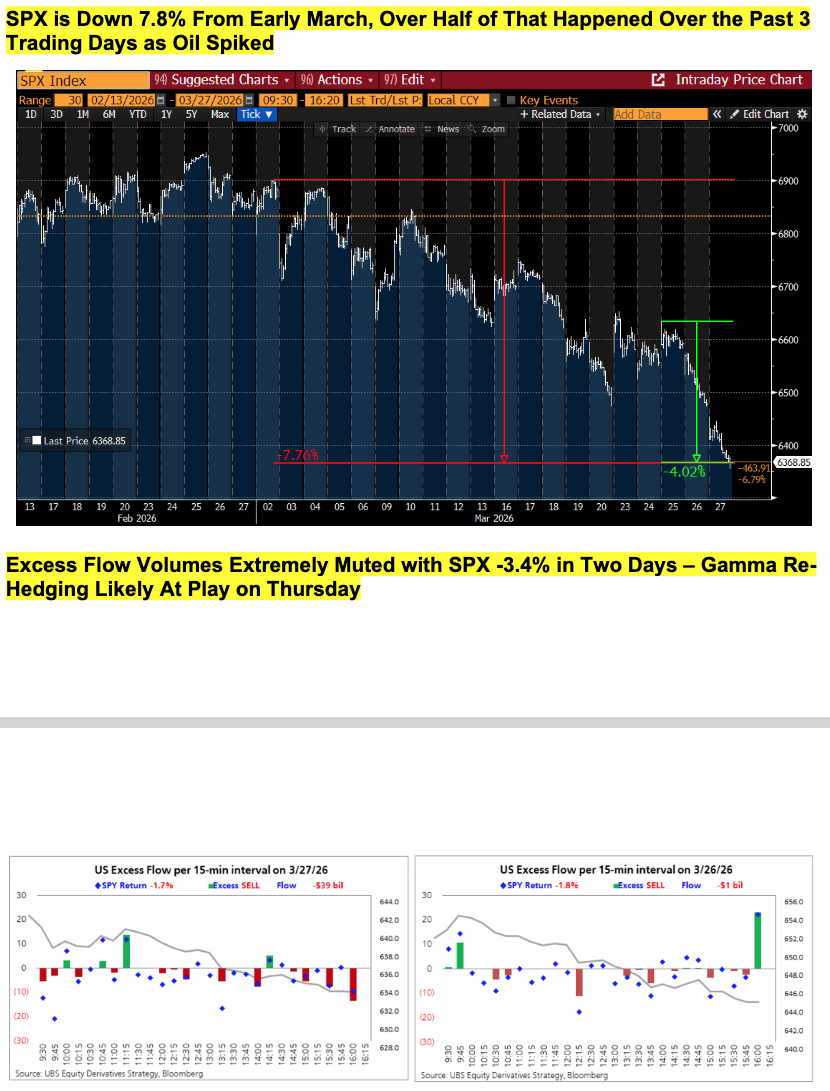

SPX is now down 7.8% from its early-March highs, with more than half of that drawdown occurring in the last three sessions as oil surged.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!