S&P500 Trading Update 1/5/26

S&P500 Trading Update 1/5/26

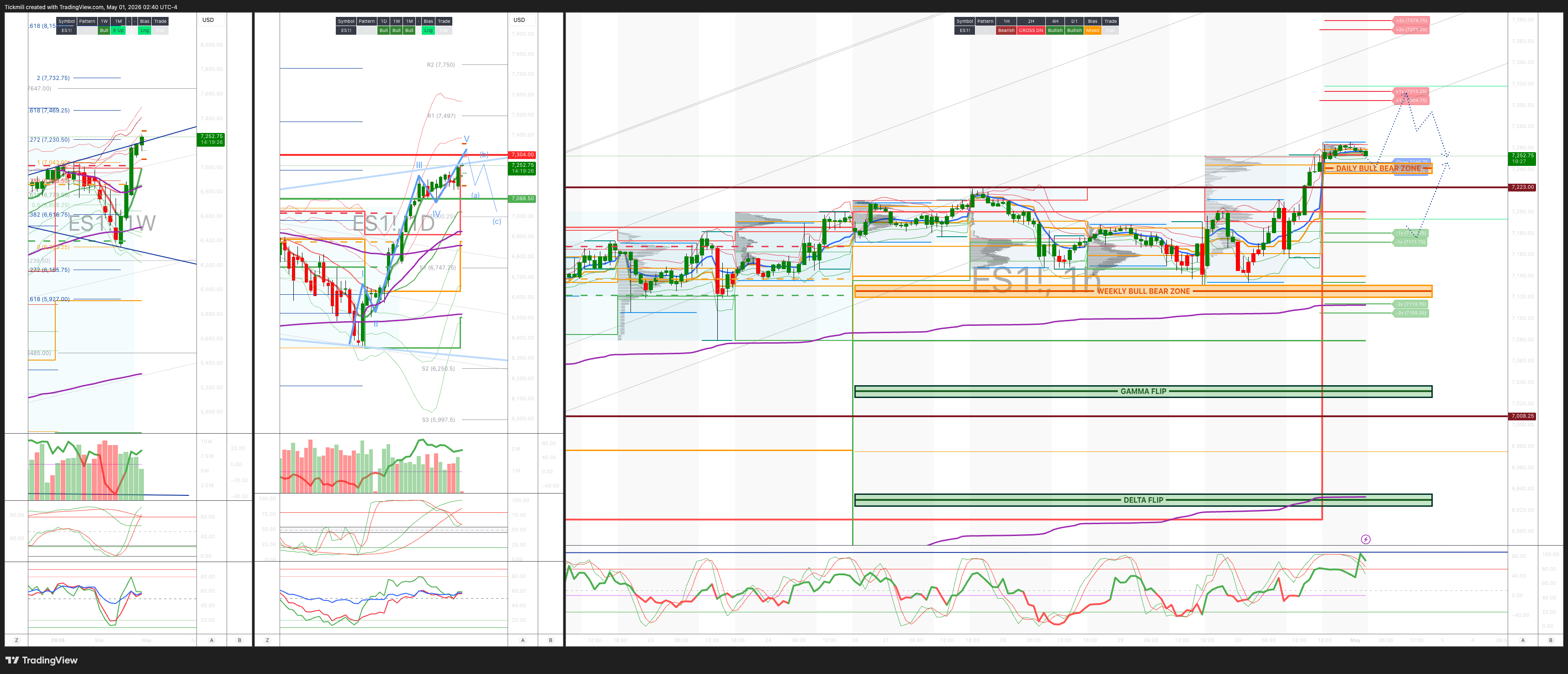

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7130/20

WEEKLY RANGE RES 7304 SUP 7087

May OPEX Straddle: 225pt range implies a OPEX to OPEX range of [6900, 7350]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.03 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BEARISH 7183

WEEKLY VWAP BULLISH 6819

MONTHLY VWAP BULLISH 6815

DAILY STRUCTURE – OTFH - 7157

WEEKLY STRUCTURE – OTFH - 7079

MONTHLY STRUCTURE - BALANCE - 7251/6359

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7245/35

GAMMA FLIP 7031

DELTA FLIP 6881

DAILY RANGE RES 7304 SUP 7171

2 SIGMA RES 7371 SUP 7105

VIX BULL BEAR ZONE 19.5

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET DAILY > WEEKLY RANGE RES

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Peak Earnings’

US Market Wrap — Broad Rally, But Under-the-Hood Rotation Matters

US equities rallied broadly, with the S&P 500 +102bps to 7,209, NDX +98bps to 27,452, R2K +220bps to 2,800, and the Dow +162bps to 48,652. Volumes improved but remain below trend at 17.2bn shares versus a 19bn YTD average, and the close saw a meaningful $3bn MOC buy imbalance. Cross-asset helped: WTI -1.1% to $105.68, 10Y yields -5bps to 4.37%, DXY -88bps to 98.09, and VIX -10.2% to 16.89. Gold rose 1.5% to $4,616, while Bitcoin gained 0.9% to $76,338.

The headline index move was strong, but the more important signal was dispersion and rotation. Megacap price action largely tracked positioning and expectations: GOOGL +10% and AMZN +1% worked, while MSFT -3.5% and META -9% lagged. This was a classic “travel and arrive” setup after a huge pre-earnings run, especially with GOOGL/AMZN up roughly 30% into prints and investors forced to digest another step-up in AI capex. The market is still willing to reward visible AI revenue acceleration, but it is no longer blindly paying for all AI spend.

Key Trading Takeaways

1. Index strength is real, but leadership is narrowing again

The S&P broke higher with a large MOC buy imbalance, lower yields, softer dollar and lower oil. That is a constructive combination. But single-stock flows were more muted than the index move suggests, and the floor described some investor paralysis given the number of earnings prints.

Trading takeaway:

Stay constructive on index momentum near term, but avoid assuming broad sponsorship. This is still a stock-pickers’ tape, not a clean “buy everything” tape.

Best expression:

Prefer relative value and dispersion over outright beta chasing.

2. GOOGL is the cleanest megacap winner; META is now the capex cautionary tale

GOOGL +10% was the standout because the print delivered enough growth validation to justify the pre-positioning. AMZN +1% was also acceptable, but less clean given heavy focus on capex and Trainium commentary. MSFT -3.5% was more nuanced: solid numbers, but investors are wrestling with pricing-model evolution between seat-count and usage-based monetization. META -9% showed the market is becoming less forgiving of AI capex where ROI visibility is less immediate.

Trading takeaway:

The market is separating AI monetizers from AI spenders.

Favor names where AI is tied to visible revenue/backlog/usage.

Be careful with names where capex is rising faster than near-term monetization.

Do not assume “AI capex up” is automatically bullish anymore.

3. Software vs semis reversion risk is rising

Software underperformed during the cash session, hurt by mixed earnings reactions and MSFT weakness. But post-close prints point to possible reversal:

TEAM +17–22% after a large beat/raise, despite being -58% YTD into print.

FIVN +22%

TWLO +11%

Meanwhile memory/momentum is cracking:

SNDK -7% to -9%, after being +336% YTD into print

WDC -6%, after being +152% YTD

Trading takeaway:

Watch for a software catch-up / memory fade trade tomorrow.

Potential expression:

Long beaten-up software winners versus short extended memory/momentum names. The setup favors mean reversion in “wrong-way” earnings movers.

4. Semis are no longer one trade

Semis were jumpy: NVDA -4% versus AVGO +3% and MRVL higher. The key debate is shifting from “AI semis all win” to merchant GPU versus custom ASIC/XPU winners. AMZN’s call highlighted Trainium strength, including more than $225bn of revenue commitments, reinforcing the idea that hyperscalers want cost leverage and vertical control.

Trading takeaway:

The semi trade is fragmenting.

Custom silicon / ASIC beneficiaries can outperform.

Merchant GPU winners may face more narrative pressure even if the overall AI pie remains large.

Avoid using broad semi beta as the only AI expression.

Best expression:

Prefer AVGO/MRVL-type custom silicon beneficiaries versus crowded merchant/memory momentum, especially after extreme YTD moves.

5. Small caps finally participated — but confirm with rates/oil

The R2K +220bps outperformed strongly, helped by lower yields and a modest oil pullback. That said, small-cap strength needs confirmation from the macro complex. If oil resumes higher or yields push back toward recent highs, the move can fade quickly.

Trading takeaway:

Small-cap upside is tradable, but not yet durable unless 10Y yields stay contained and oil stops pressuring inflation expectations.

Potential expression:

Use call spreads rather than outright long beta in RTY/IWM until the rates backdrop stabilizes further.

6. Consumer bounce still looks low quality

Despite the modest pullback in oil, the consumer bounce felt more like abatement of supply than genuine buying. The desk noted no real buyers in the space.

Trading takeaway:

Be skeptical of consumer-discretionary strength unless flows improve. Lower oil helps at the margin, but positioning/fundamental conviction still appears weak.

Fade candidates:

Consumer rallies without volume, upgrades, or clean earnings support.

7. Apple was solid, but not a clean catalyst

AAPL -1% post-close despite a solid print:

EPS beat by 5c

Revenue $111.2bn vs $110bn consensus

iPhone revenue roughly in line at $57bn

Services beat at $31bn vs $30.3bn

China revenue beat at $20.5bn vs $18.9bn

“Extraordinary demand” for iPhone 17

March-quarter iPhone revenue record

$100bn buyback authorization and dividend increase

The issue is positioning. The desk had AAPL at 7/10, and length appears to have crept up as an AI hedge, even though many remain under-owned relative to its roughly $4trn market cap.

Trading takeaway:

Apple’s print is fundamentally fine, but the stock may not provide enough upside surprise to lead the index higher immediately. It is more likely a stabilizer than a fresh accelerator unless the call delivers stronger AI or China commentary.

Derivatives Takeaways

Vol did not confirm the equity rally

Despite SPX gaining more than 1%, vol closed little changed. NDX vol was offered across the curve, while skew relaxed in both SPX and NDX. The desk expects small rallies to see fixed-strike vol float as the hurdle resets lower.

Trading takeaway:

The market is still not paying up for upside convexity. Rallies are being absorbed by lower implieds and relaxed skew.

Hedges are being added on strength

Flows were quieter, but the desk saw more hedging into the rally, especially SPY put spreads in end-May and regular June maturities.

Trading takeaway:

Investors are not fully embracing the rally — they are using strength to add defined downside. That supports the view that upside can continue tactically, but conviction remains limited.

Preferred hedge:

Put spreads over outright puts, given vol is not exploding and dealer gamma remains relatively stabilizing.

Weekend/event risk looks underpriced

The straddle through Monday’s close is less than today’s SPX move, and the end-week straddle sits at 0.56%.

Trading takeaway:

Short-dated implieds look complacent relative to realized moves and the macro/earnings backdrop. If carrying gamma, own it selectively where realized can stay elevated; if selling vol, be disciplined and avoid event-heavy single names.

Flow Takeaways

Asset managers and hedge funds were not aggressively buying

Asset managers finished roughly $1bn better for sale, driven by supply in Information Technology, Consumer Discretionary and Communication Services, offset by demand in macro products. Hedge funds were small net sellers, with supply in Technology, Industrials and Energy, offset by demand in Consumer Discretionary and Communication Services.

Trading takeaway:

The index rally was not matched by a strong discretionary sponsorship signal. That makes the move more vulnerable to reversal if macro support fades.

Post-Close Movers to Watch

Positive

TEAM +17–22%: major beat/raise; key software reversion candidate.

FIVN +22%: software squeeze.

TWLO +11%: another beaten-down software winner.

ROKU +10%: beat and raise FY outlook.

MPWR +7%: revenue beat, $804mn vs $783mn consensus.

RIVN positive: EBITDA beat; likely modest positive.

Negative

RBLX -18%: large cut to FY bookings guide.

SNDK -7–9%: guidance still strong, but deceleration versus prior sequential growth guide matters after extreme YTD move.

WDC -6%: sympathy/memory momentum unwind.

FND weaker: EPS miss, comp miss, and EPS guide cut.

AAPL -1%: solid but not enough versus positioning.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!